Leominster Credit Union

SavvyMoney®

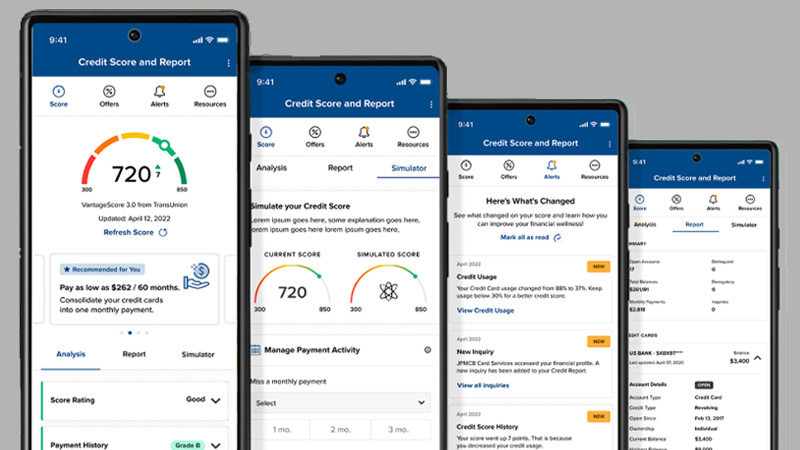

Credit Score. And More.

It’s easy to get started:

- Log into Mobile or Online banking

- Click SavvyMoney® button "Get my Score"

- Enroll to activate

And it's free!

Benefits of SavvyMoney®

- Daily Access to your Credit Score

- Real Time Credit Monitoring Alerts

- Credit Score Simulator

- Personalized Credit Report

- Special Credit Offers

- And more!

Frequently Asked Questions

What is SavvyMoney® Credit Score?

What is a Credit Score?

A credit score is a three-digit number calculated to indicate your creditworthiness. The higher the score, the more creditworthy you are to a lender. A credit score is calculated from the information in your credit report and considers your on-time payments, the length of your payment history, your mix of different types of credit accounts, and other such factors. It is important to know that your score does not take your age, income, employment, marital status, or your bank account balances into account.

You can learn more about credit scores and scoring models from the Consumer Financial Protection Bureau website: https://www.consumerfinance.gov/ask-cfpb/what-is-a-credit-score-en-315/

What is VantageScore®*?

VantageScore® was founded by the 3 leading credit reporting agencies – Experian, Equifax, and TransUnion. This credit score model was developed by a representative team of statisticians, analysts, and credit data experts from each of the credit reporting companies, and is used by hundreds of institutions, including credit unions, banks, credit card issuers, and mortgage lenders.

The VantageScore® 3.0, the score that is shown in SavvyMoney®, is a newer and more popular version of VantageScore®. It is calculated on a scale of 300-850, with 300 being the lowest and 850 the highest score.

*Please note that your credit score and the rate shown use the TransUnion Vantage 3.0 scoring model and will differ from the Experian scoring model used in our standard underwriting. Offers are not pre-approvals or offers to lend to you. You still must apply with Leominster Credit Union. A credit report is pulled at the time of application, and LCU uses an Experian credit score to review applications and make lending decisions. Actual loan rates and terms will be determined when you apply for credit.

Offers are calculated by comparing your credit profile from a soft credit pull to the general criteria determined by Leominster Credit Union. A soft credit pull quickly checks your credit to generate offers and does not affect your credit score. If you choose to apply, a hard credit pull will be conducted, which may affect your credit score. Rates are based on creditworthiness and other factors and may be higher than the rate shown. Rates and terms are subject to change without notice. All loans are subject to credit approval.

What Does a "Good" Credit Score Mean to Me?

A good score may mean you have easier access to more credit and lower interest rates. The consumer benefits of a good credit score go beyond the obvious. For example, underwriting processes that use credit scores allow consumers to obtain credit much more quickly than in the past.

What Factors Influence My Credit Score?

Five major categories make up a credit score:

- 40% Payment History

Essentially, lenders want to know whether you’re good about paying your loans on time. - 23% Credit Usage

Credit usage, also known as credit utilization, is the ratio between the total credit used and your total credit limit on your revolving accounts. It is best to keep your credit usage below 30%. - 21% Credit Age

The average of your oldest open credit accounts to your newest open credit accounts determines your credit age. In general, the longer your credit history the better, particularly accounts with a good payment history and no late payments. - 11% Credit Mix

It’s important to have a mix of different types of credit like revolving credit and installment loans. Your score will likely be higher if you have a good payment history with both, installment loans, like student loans and mortgages, and revolving credit, like credit cards. - 5% Inquiries

Any time you apply for a credit card, or a lender checks your credit for a loan, it’s known as an inquiry. Hard inquiries show on your credit report when your credit is pulled by a lender for a car loan, mortgage, or credit card. However, soft inquiries don’t show on your credit report and occur when you check your credit, or a lender pre-approves you for an offer.

Applying for several credit cards or opening multiple credit accounts in a short period creates hard inquiries and could signal an increased credit risk to a lender.

Do race, age, and other, non-credit related factors affect my VantageScore® credit score?

One of the most important misperceptions about credit scores is what information the VantageScore® model, or any credit scoring model for that matter, is NOT used. The VantageScore® model does not consider race, color, religion, nationality, sex, marital status, age, salary, occupation, title, employer, employment history, where you live or where you shop.

What is SavvyMoney® Credit Report?

What is a Credit Report?

Credit reports, also known as credit files, are composed of the credit-related data a credit reporting company has gathered about consumers from different sources. Credit reports include records of mortgage payments, credit card balances, credit card payments, auto loan payments, and credit inquiries. It may also include accounts that have gone into collections, public records, and other information from government sources.

Credit reports include the following about your debt accounts:

- A list of creditors that have extended credit or loans.

- Total loan amounts and credit card limits.

- Payment amount and history on all loans and credit lines.

Credit reports may also include:

- Inquiries, each time your credit report was pulled by a lender in the past 2 years.

- Your current and/or former address(es)

- Your current and/or former employers

- Other details of public record

Under Federal law, you are entitled to receive one free copy of your credit report from each credit reporting agency every 12 months. You can obtain a free copy of your credit reports at https://www.annualcreditreport.com or by calling 1-877-322-8228. For more information visit https://www.consumerfinance.gov/ask-cfpb/what-is-a-credit-report-en-309/

How Can I See What’s in My Credit Report?

Not sure about what’s in your credit report? Click over to “Credit Report” to review all your accounts, payments, and more. You can also receive a free Credit Report from each of the credit reporting companies – Equifax, Experian, and TransUnion once a year.

How Do I Correct My Credit Report if I Think There’s an Error?

Given this incredible volume of data provided by lenders to the agencies, there are times when the information reported about your credit activities may be inaccurate.

If you find information that you believe is not correct on your credit report, contact the company that issued the account or the credit reporting company that issued the report. You can dispute any inaccuracies found on your TransUnion credit report by navigating to the bottom of the SavvyMoney® Credit Report and clicking “dispute”.

For more information visit: http://www.consumerfinance.gov/askcfpb/313/what-should-i-look-for-in-my-credit-re port-whatare-a-few-of-the-common-credit-report-errors.html

Why Don’t My Free Credit Reports Include My Credit Scores?

Your credit report and score are different. Your credit report is all the information that a credit reporting agency has gathered about you. Credit reporting agencies calculate your credit score by plugging the information in your credit report into their proprietary credit score formula.

Federal law gives you the right to ask for a copy of your credit report from each nationwide credit reporting company every year for free. However, the law does not require credit reporting companies to give your credit score for free.

For more information visit https://www.consumerfinance.gov/ask-cfpb/i-got-my-free-credit-reports-but-they-do-notinclude-my-credit-scores-can-i-get-my-credit-score-for-free-too-en-6/

What is a Credit Freeze?

A credit freeze, also known as a security freeze, is a free way to restrict access to your credit report. Adding a freeze means no one, not even you, can open a new credit account while the freeze is in place. You can, however, temporarily remove this freeze at any time if you want to apply for new credit.

It is important to note that a credit freeze does not affect your credit score. While the freeze is in place, you will still be able to apply for a job, rent an apartment, purchase insurance, and receive pre-screened offers.

How to Place a Credit Freeze?

To place a credit freeze on your credit profile, you must contact each of the three major credit bureaus:

- TransUnion - Phone: (888) 909-8872 / Web: Credit Freeze | Freeze My Credit

- Equifax - Phone: (888) 298-0045 / Web: Security Freeze | Freeze or Unfreeze Your Credit Equifax®

- Experian - Phone: (888) 397-3742 / Web: Security Freeze | Experian

How to Unfreeze Your Credit Profile?

You must contact the three major credit bureaus to unfreeze your credit profile. Each bureau has a different process, but each will initially provide you with a PIN to unfreeze your profile.

Who uses credit scores for lending?

Do Only Banks and Lenders Use Credit Scores?

Any institution that lends money – credit unions, banks, credit card companies, financing companies, mortgage lenders, and others – can use a credit score to help them assess whether you meet their lending criteria. These institutions use your credit score along with other relevant information provided by you, such as income, work status, and down payment amount. In general, higher scores allow access to more credit at competitive rates.

Insurance carriers can also use credit scores to help assess risk and to accurately price homeowners and automobile insurance policies.

Is Credit Score the Only Thing Used by Lenders for Loan Approval?

No, a credit score is just one part of several factors lenders use in their lending criteria. Other lending criteria considered may include:

- Loan-to-Value Ratio

- Income

- Current employment and work history

How do I improve my credit score and build credit?

How Do I Improve My Credit Score?

There are several ways to improve your credit score. However, it’s much more important to focus on improving what’s in your credit report rather than over your credit score. Here are some quick tips to help:

- Pay Your Bills on Time, Every Month. Payment history is the largest factor in your credit score.

- Apply for Credit Only When You Need It. Try not to open too many accounts too frequently. These frequent inquiries can ding your credit.

- Keep Your Outstanding Balances Low. Keep balances below 30 percent of the credit limit on each of your revolving accounts.

- Reduce Your Total Debt. It is not necessarily bad to have debt as long as it’s manageable. Too much debt at high interest rates can get out of hand if a financial emergency comes up. Consider paying down some of your outstanding loans.

- Build Up Credit History. Maintaining a timely payment history for a mix of accounts (e.g. credit cards, auto, mortgage) over a long period can improve your score.

Should I Carry a Balance on My Credit Cards Each Month or Pay the Cards in Full Each Month?

Since the single most important factor in credit score is payment history, using credit and paying off your balances on time will have the greatest impact on your score. Carrying a balance every month may incur interest charges, so if you can, pay off the cards in full and on time.

The best way to build a solid credit score is to manage all your accounts properly. Best practices include paying all your credit obligations on time every month, applying for credit only when needed, and keeping balances on credit cards as low as you possibly can if you cannot pay them in full each month.

Are Charge Cards Treated the Same as Credit Cards by Credit Scoring Models?

A charge card is like, but not the same as, a credit card. As such, there are subtle differences in how they’re used in credit scoring.

Typically, a charge card balance is due in full each month, while credit card balances can be carried, or "revolved," from month to month. Charge cards do not have published credit limits, whereas credit cards do.

Charge card accounts factor into credit scores but are not used by the VantageScore® scoring model, due to the lack of a credit limit used in calculating "balance to credit limit" measurements.

If I Close My Credit Card Accounts, Will That Improve My Score?

When you close a credit card account, you lose the value of that card’s credit limit in the credit usage calculation. The credit limit is an important component when determining a consumer’s balance to credit limit or the “credit usage” ratio. This ratio rewards consumers who have low credit card balances relative to their credit limits.

If you close credit cards, especially those with large credit limits, you will likely cause your credit usage ratio to go up (if you carry balances). This can cause your score to go down considerably.

Additionally, if you close credit card accounts the credit bureaus will eventually remove them from your credit reports. Even though it can take years for an account to be removed from your credit reports, once it is gone you will get no credit for your responsible management of that account.

Is Medical Debt a Factor in My Credit Score?

Medical bills are usually not reported to the credit bureaus unless they have been unpaid for a long time and have gone to collections. Collections accounts stay on the report for as long as 7 years even after you’ve paid them off. These accounts typically hurt scores, though some scoring models do not include medical collections, especially those with small balances of less than $100. VantageScore® 3.0 does not take paid collections accounts into account in its model.

Source: https://www.vantagescore.com/newsletter/your-score-vs-medical-debt/

Will My Credit Score Be Higher the More Loans I Have?

The quantity of loans is not as important in credit scoring as the quality of how well those accounts are managed. In other words, your score is more positively impacted by keeping loans in good standing without missing payments.

Does Shopping for a Loan Hurt my VantageScore®?

Consumers are encouraged to shop for the best loan rates and conditions. Accordingly, the VantageScore® model does not penalize multiple inquiries made within a short period. When several inquiries are made within a shortened timeframe, it is assumed that the consumer is shopping around for a rate and not opening multiple lines of credit.

The VantageScore® model uses a 14-day rolling window in which all credit inquiries within that window are considered one inquiry regardless of the type of account. So regardless of whether the credit inquiry is made in response to a mortgage, auto, or bank credit card application, it will be counted only once during that 14-day window.

Is it True the Fewer Credit Cards the Higher My Credit Score?

Credit reports reflect your credit activity. The quantity of cards is less important than how you manage your credit cards. It’s generally a good idea to have a limited number of credit cards so that you can keep low balances, with a good payment history, over a long period.

If I Have a Credit Balance on My Cards, Will My VantageScore® Improve?

Credit balance does not positively or negatively impact credit score.

If I Pay Off My Credit Card Debt, Will My Credit Score Get Better?

Paying off debts does not automatically boost your score. While your credit card and other loan balances may be low because of a recent payment, due to the lenders’ reporting cycles, it may take some time for the payments to be reflected in your credit score. Moreover, available credit and balances are only one of several other factors that are considered by credit score models. Improving your credit score can be achieved over time by regularly practicing these sound financial management techniques:

- Pay your bills on time

- Apply for credit only when it’s needed; do not open new accounts frequently or open multiple accounts within a short period.

- Keep your outstanding balances low – a good rule of thumb is not to exceed 30% of your available credit limit with each account.

- Pay any delinquent accounts as soon as possible and then keep them current.

If I Carry a Balance on My Credit Card, Will it Help Me Build Credit More Quickly Than Paying in Full Each Month?

Not necessarily. The balance of an account does not affect the speed at which you will build or re-build your credit scores. A credit card with a $5,000 balance ages just as quickly as a credit card with a $0 balance. Further, even if you pay your balance in full each month there’s no guarantee that the account will show up on your credit reports with a $0 balance. Credit card issuers report your statement balance to the credit reporting agencies. That means even if you pay your balance in full any subsequent use of the card is going to result in a statement balance greater than $0.

One of the most effective ways to build or rebuild your credit is by responsibly managing your accounts. Maintaining low balances on credit cards and never missing a payment will lead to better credit scores.

When I Close a Credit Card Account, Will My Credit Score Go Down?

Your credit score may go down if you close a credit card account. The reason your score drops would be due to the loss of the credit limit of the closed card in your debt-to-credit limit ratio measurements.

If you carry a balance on other credit cards then your debt-to-limit ratio, calculated by dividing your aggregate credit card debt by your aggregate credit limits on open credit cards, will likely go up. This may cause your credit score to drop.

If you don’t carry a balance on other credit cards or the credit limit on the newly closed card was modest enough, then the account closure may not result in a change in your debt-to-limit ratio sufficient to result in a score reduction.

If I Pay Off Loans or Close Credit Cards, Will They Be Removed from My Credit Report?

The credit reporting agencies do not remove accounts once they’ve been closed or paid off. There is no law requiring credit reporting agencies to remove accounts that are in good standing. At this time, however, the credit reporting agencies choose to remove inactive or closed accounts 10 years after they’ve been closed. Additionally, while closed or paid-off accounts are still on your credit reports they are still considered in credit scoring.

If I Don’t Have a Long Credit History, Can I Still Get a VantageScore®?

One of the differentiating factors of the VantageScore® models is the ability to calculate scores for more consumers, which includes those who are new to the credit market, infrequent credit users, or those who have two or fewer credit accounts.

The VantageScore® models are more likely to provide a score for consumers who are very new to credit and have less than 6 months of history. They also score those with activity up to two years ago on at least one of the accounts in their file.

Will LCU use SavvyMoney® Credit Score to make loan decisions?

No, LCU uses its own lending criteria for making loans.

How often will my credit score be updated?

As long as you are a regular online banking user, your credit score will be updated periodically and displayed in your online banking screen. You can click “refresh score” as frequently as every day by navigating to the detailed SavvyMoney® site from within online banking.

How does SavvyMoney® Credit Score keep my financial information safe?

SavvyMoney® uses high-level encryption and security measures to keep your data safe and secure. Your personal information is never shared with or sold to a third party.

Is there a fee?

No. SavvyMoney® is entirely free and no credit card information is required to register.